BANGKOK — Fried chicken vendor Sontaya Mookon, 39, described his debts over the past year as dried layers of dirt caked on a pig’s tail, using a Thai idiom that means “to keep increasing.”

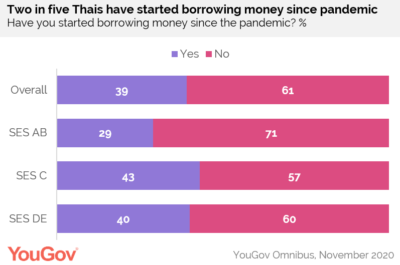

Sontaya is the owner of Toh Jeen Fried Chicken food stall. He said he went deep into debt since the coronavirus broke out in January, and only managed to have some money to pay it back by selling at recent pro-democracy protests. His experience is far from unique – two out of five Thais may have overborrowed in the pandemic, according to a new survey.

“I couldn’t get any money during COVID. I’m just a cart, so wherever I go, City Hall officials would chase me away,” Sontaya said. “My finances went into the negative.”

A survey compiled by London-based YouGov said lower-income households and middle aged Thais between 35 to 44, like Sontaya, were more likely to borrow money than any other group.

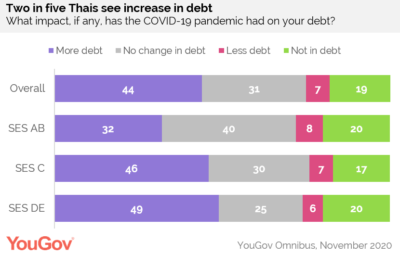

Although household debts have always been a problem in Thailand, the matter appears to be made worse by the coronavirus. YouGov found that eight in ten Thais are currently in debt, and more than two in five said they have more debt since the pandemic began.

About two in five said they were spending less overall, but a similar number of respondents said they ended up paying more amid the outbreak.

Food and beverages, housing, and personal care are listed among the items people tend to spend more money on, but less so on clothing, entertainment, and electronics.

Nonarit Bisonyabut, a macroeconomics expert at the Thai Development Research Institute, or TDRI, said the YouGov survey may not account for the super-rich and people with a monthly income of at least 100,000 baht, but he believes the report paints a accurate picture for the middle and lower classes.

“COVID affects people with incomes of less than 60,000 baht per month anyway,” Nonarit said. “The sector of the population with no savings and high debt are already vulnerable, but with COVID, they’re now trapped in a hole of debt.”

Leaving Some Behind

Sontaya, the fried chicken vendor, said he already incurred some debts from the past couple of years due to “necessary expenses.” But his money situation went downhill when lockdown measures were introduced earlier this year due to the coronavirus, he said.

Travels were discouraged, businesses shut down, and tourists barred from entering Thailand save for a very few.

“I would make as little as 600 baht per day,” said Sontaya, who sold the chicken in Siam area at the time. “Of course I was in the negative. Debt became like dried dirt on a pig’s tail.”

During the pandemic, the government proposed several handout programs, most notably the “No One Left Behind” initiative, which could be applied for through the social security system. Farmers, people living with disabilities, and the elderly were also eligible for separate handout programs.

But “No One Left Behind” proved to be somewhat of a shortfall. The cash handout – 5,000 baht for three months – is too little for many, and some applicants who qualified for the program never got the money, leading to a protest at the finance ministry in April.

“In the end, no one was paid more than 5,000 baht for three months. Honestly, no one can survive on that,” Nonarit said. “Therefore, this resulted in lots of people borrowing money and going into debt.”

He added, “The only people exempt from this are people with enough savings for 6 months or a year. Very few Thais have enough to do that.”

Uncertain Future

Thais often turn to their families first when they need to borrow, and if that fails, their friends.

Sontaya said he had owed money to his chicken supplier and his mother. When buying chicken from the supplier, he would owe 3,000 baht to 4,000 baht with each shipment since he didn’t have cash to pay for them. His mom would then send him both money and food from the upcountry to help him get by.

Many also turn to informal loan institutions, from pawn shops to loan sharks. These loans come with interest rates much higher than the commercial banks, such as 36 or even 48 percent. Loans approved by the banks generally have an interest of 24 percent, Nonarit from TDRI said.

Although most of those surveyed in YouGov said they borrowed from banks (57 percent), a third borrowed via credit card (33 percent), family and friends (28 percent), and “informal loans” (21 percent).

“COVID increases uncertainty for people, who don’t know what their future looks like,” Nonarit said. “Paying off things like a car or motorcycle needs a steady stream of income.”

Sontaya said most of his income goes to his 7,000-baht rent, car payments, and expenses of providing for his family. “I’m very careful with my money. I never go anywhere; I just work for my family,” he said.

Fortunately enough for him, the series of anti-government protests that began in July and escalated in October provided him with new venues to sell the fried chicken and pay back some of his debts. At each rally, Sontaya said, he made almost 9,000 baht a day, compared to the average of 1,500 baht per day when there were no protests.

“I’m really happy to get this money,” he said. “I began to have savings of 10,000 baht, after being more than 40,000 baht in debt.”

But Sontaya said his financial situation remains tenuous since he relies on the sporadic rallies for customers, and no one knows how long the protests will last. “I don’t know what my future will be like,” he said. “I have savings, but to be honest, I only have 14,000 baht to my name right now.”

The YouGov survey was conducted on 2,083 Thais between Nov. 23 and 26 in return for compensation and is representative of the online population. The margin of error is 3 percent.

Thailand’s gross domestic product, or GDP, also shrank 6.4 percent in July-September compared to a year ago, according to the National Economic and Social Development Council.

{kind=link}