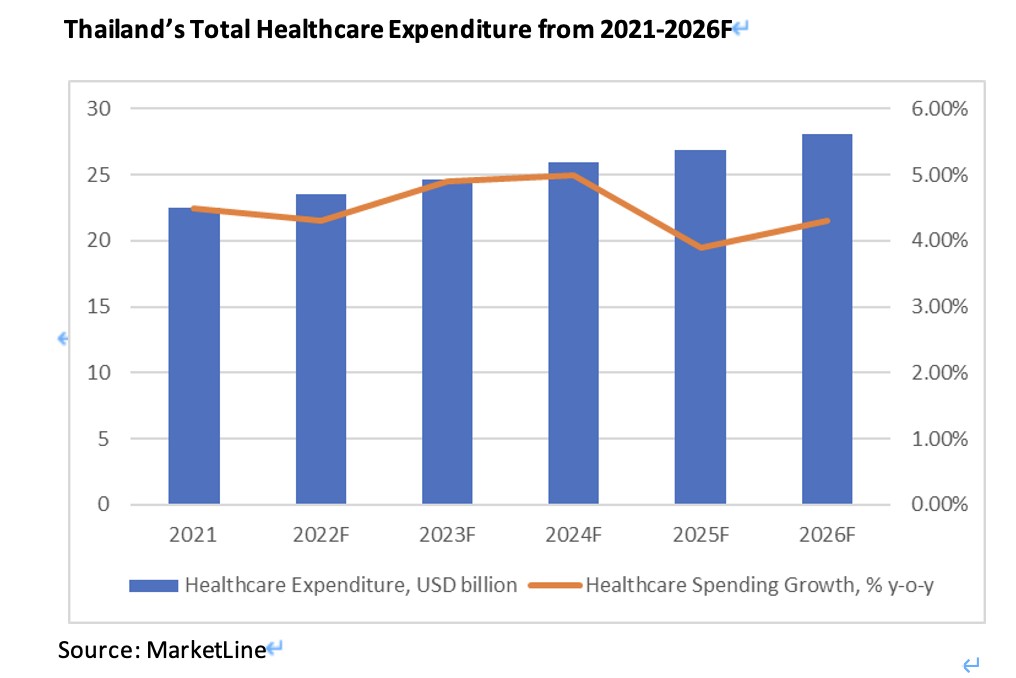

Thailand’s healthcare spending in 2021 was USD 22.5 billion, representing a compound annual growth rate (CAGR) of 5.7% from 2017 to 2021. The healthcare sector in Thailand constitutes 4.5% of the country’s GDP, with a per capita spending of USD 306.

The private side contributed 26.6% of the total health expenditure, while the government contributed 73.4%. The COVID-19 pandemic has led to a significant increase in the in-patient and medical goods segment, while out-patient care segment declined as patients deferred care amid disruptions in healthcare provision.

It is expected that the healthcare sector growth is going to slow down, with a CAGR of 4.5% from 2021 to 2026 with a total value of USD 28.1 billion achieved by 2026. The aging population is expected to drive demand for advanced medical interventions, with healthcare costs for the elderly projected to triple by 2032.

The public sector contributed 73.4% of the total healthcare expenditure in 2021 to reach USD 16.5 billion. There were 13,364 government medical facilities in Thailand, accounting for 34.7% of all healthcare facilities in Thailand. Among all the public medical facilities, 294 of are secondary and tertiary care facilities. Hospitals with quaternary care and strong research capabilities are another focus of the public healthcare sector.

The public sector made up of 65.3% of all healthcare facilities in Thailand. There are 370 private secondary or tertiary hospitals in the country with 31.4% located in Bangkok and 68.6% in other provinces. The bed occupancy rate from private healthcare facilities is 61% which is less crowded than public facilities. Due to the government healthcare system’s inability to keep up with the increasing demand, private hospitals have attracted many middle-class consumers.

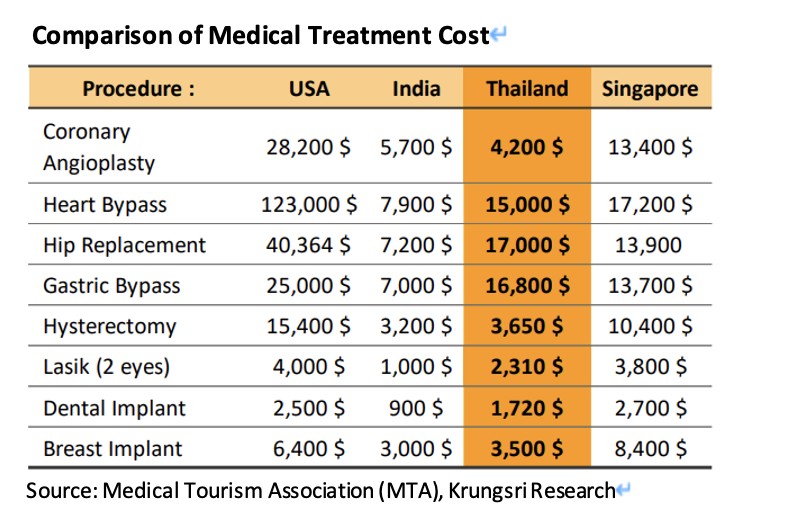

In addition, the relatively lower cost of medical treatment of private hospitals compared to developed countries has made them a popular destination for medical tourism. Private hospitals in Thailand cover a wide range of customers, from high income international patients to general patients covered by the Social Security Scheme.

In terms of healthcare insurance, public healthcare insurance covered over 99.3% of eligible citizens. The three main health insurances in Thailand are: Universal Coverage Scheme (UCS), Social Security Scheme (SSS), and Civil Servant Medical Benefit Scheme (CSMBS). As of 2019, out-of-pocket payments made up 8.7% of the total healthcare expenditure in Thailand, a significant decrease from 34% in 2001. Voluntary health insurance contributed to 14% of the total healthcare expenditure.

For healthcare provision, Thailand had a total of 38,512 healthcare facilities as of 2020, with 34.7% operated by the government and 65.3% privately owned. 98.3% of the facilities were primary care facilities while 1.7% were secondary and tertiary hospitals. Despite the large number of hospitals in Thailand, there is still a significant disparity in healthcare access and quality between urban and rural areas.

For healthcare workforce, Thailand had 38,820 doctors and 184,840 nurses as of 2022, with an average ratio of 0.60 doctors and 2.83 nurses per 1000 people in the country. Similar to healthcare facilities, there is a regional disparity in personnel allocation. To address this issue, Thai doctors are required to serve in the public sector for at least three years after graduation at facilities assigned by the Ministry of Public Health.

Thailand’s average life expectancy was 79.7 years, the second highest in Southeast Asia after Singapore. The top four causes of death in Thailand in 2021 were cancer (14.9% of deaths), cerebrovascular disease (6.6%), pneumonia (5.9%), and Ischemic heart disease (4.0%).

Since 2003, Thailand has actively pursued its medical hub policy, aiming to become a regional leader in medical services. Despite a significant revenue drop to THB 2.9 billion in 2020 due to the pandemic, Thailand remains a top medical tourism destination, recognized for healthcare quality.

With 59 Joint Commission International-accredited facilities and competitive medical treatment costs, Thailand stands as a global hub. Private hospitals employ diverse strategies to attract global patients, and the government supports the industry through visa extensions and incentives for healthcare investments.

TTB Analytics projects Thailand’s medical tourism industry to surpass THB 25 billion in revenue by 2023, driven by exceptional healthcare management and advancements in medical technology.

In the short term, Thailand healthcare market is expected to experience a surge in demand for healthcare services from a backlog of patients who were previously waiting to receive treatment but were unable to do so due to Covid-19 protocol constraints. In the mid to long run, the country’s aging society is expected to drive the demand further.

{kind=link}