Deloitte’s latest report “The future of distressed debt in Thai capital markets”, spotlights Thailand’s distressed debt market – an evolving landscape that faces many challenges but comes with potential opportunities for growth.

The report delves into the intricacies of distressed loans and bonds – revealing insights into the market’s history; unfolding challenges from a market, regulatory, and infrastructure perspective; and key transformative initiatives based on lessons and case studies from other countries.

The 1997 Asian Financial Crisis acted as a catalyst for the distressed loan market in Thailand, pushing around 60% of the country’s financial institutions to the brink of insolvency. In response, the Thai government implemented targeted measures, including the establishment of corporate rehabilitation procedures and the introduction of Asset Management Companies (AMCs).

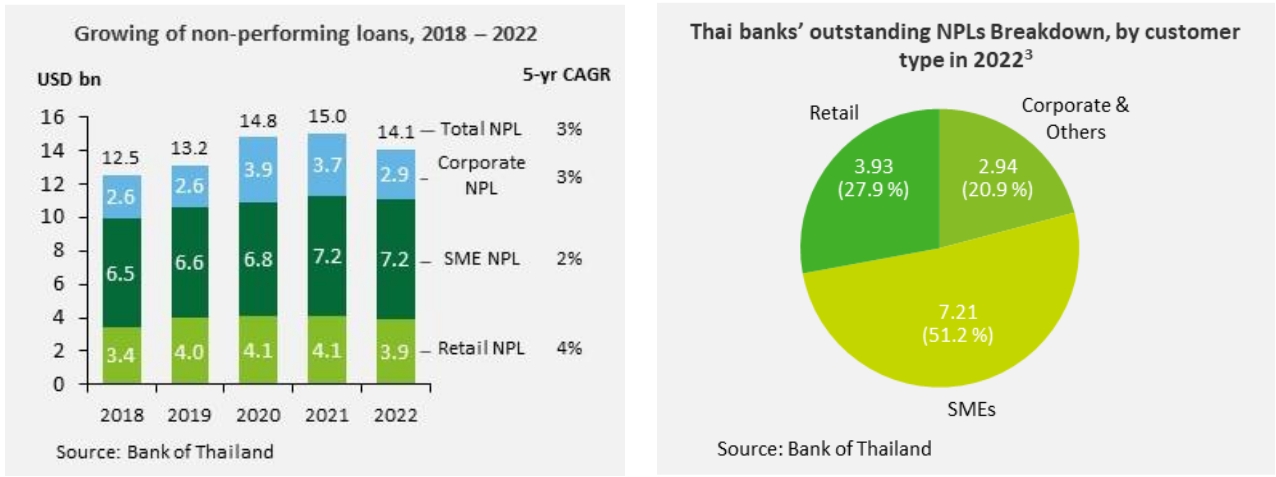

Fast forward to the present day, the Non-Performing Loans (NPLs) market is currently valued at approximately USD 14 billion, primarily comprised of SME NPLs, accounting for about 50% of the outstanding NPLs in the market.

Additionally, there has been an increase in Special Mention Loans – SML (referring to 30 to 90 days overdue loans) in recent years, growing from USD 12.3 billion in 2019 to USD 32 billion in 2023. Market experts have shared that approximately half of the SMLs within the financial institutions’ system will transition into NPLs within next 2 years, indicating potential growth in the NPLs market in the coming years.

It is important to take a note that despite the market developments since the 90s, Thailand continues to rely heavily on AMCs to resolve NPLs, while not yet embracing additional market solutions.

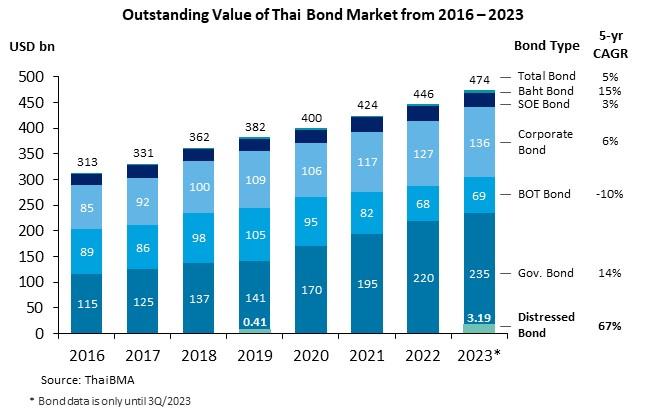

In contrast, the distressed bond market in Thailand only came into the spotlight during the COVID-19 pandemic where the market witnessed 683% growth from 2019 to 2023. However, the distressed bond market today is valued at approximately USD 3 billion, still relatively small compared to outstanding NPLs.

Key challenges for developing the distressed debt market in Thailand, as detailed in the report, include difficulties in attracting and scaling demand from new investor pools, regulatory barriers limiting new participation and investment opportunities, and a lack of supporting infrastructure and intermediaries.

The market today relies heavily on AMCs to resolve the country’s outstanding NPLs; as NPLs are expected to continue rising in the future, there is a risk that AMCs will not have sufficient capacity to handle the debt. There is opportunity for the market to attract new entrants of diverse investor pool to scale up demand and balance this risk.

Regulatory plays an important role in allowing certain distressed debt activities to increase market liquidity. Current restrictions in regulations such as type of funds allowed to invest in distressed debt, limitations on institutional investors, and barriers in rehabilitation frameworks and eligibility processes for foreclosure are some examples of challenges discussed in the report.

The Thai market also lags international counterparts in terms of attracting participation from institutional intermediaries, and fostering inter-agency collaborations to build a solid infrastructure for addressing distressed debt issues and enabling a robust market.

Based on leading practices from abroad, the report explores several initiatives from the United States, Europe, and South Korea, presenting potential options for managing distressed debt market in Thailand. These include:

- Scale demand by attracting wider range of investors to promote healthy competition and innovation in the capital markets. Implement incentive schemes such as tax schemes to attract fresh capital and increase supply of debt instruments by diversifying to new asset classes.

- Review regulations related to rehabilitation frameworks and eligibility processes for foreclosure to align more closely with market dynamics, encompassing diverse debtor archetypes and ensuring fairness to creditors. Consider easing restrictions on investment participation for institutional investors (e.g., mutual funds, insurance companies). Promote collaborative efforts through inter agency taskforce initiatives between public and private sectors to ensure clear jurisdictional alignment and drive strategic decisions holistically.

- Facilitate a resilient secondary market for debt by modernising asset transfer mechanisms such as implementation of efficient clearing and settlement systems, trading platforms, and standardisation of data and processes.

- Cultivate skilled professionals by implementing investor education initiatives in collaboration with academic institutions. Attract experienced international players to the Thai market to facilitate the exchange of knowledge and best practices to local talents.

To read the full report, visit: this link

{kind=link}